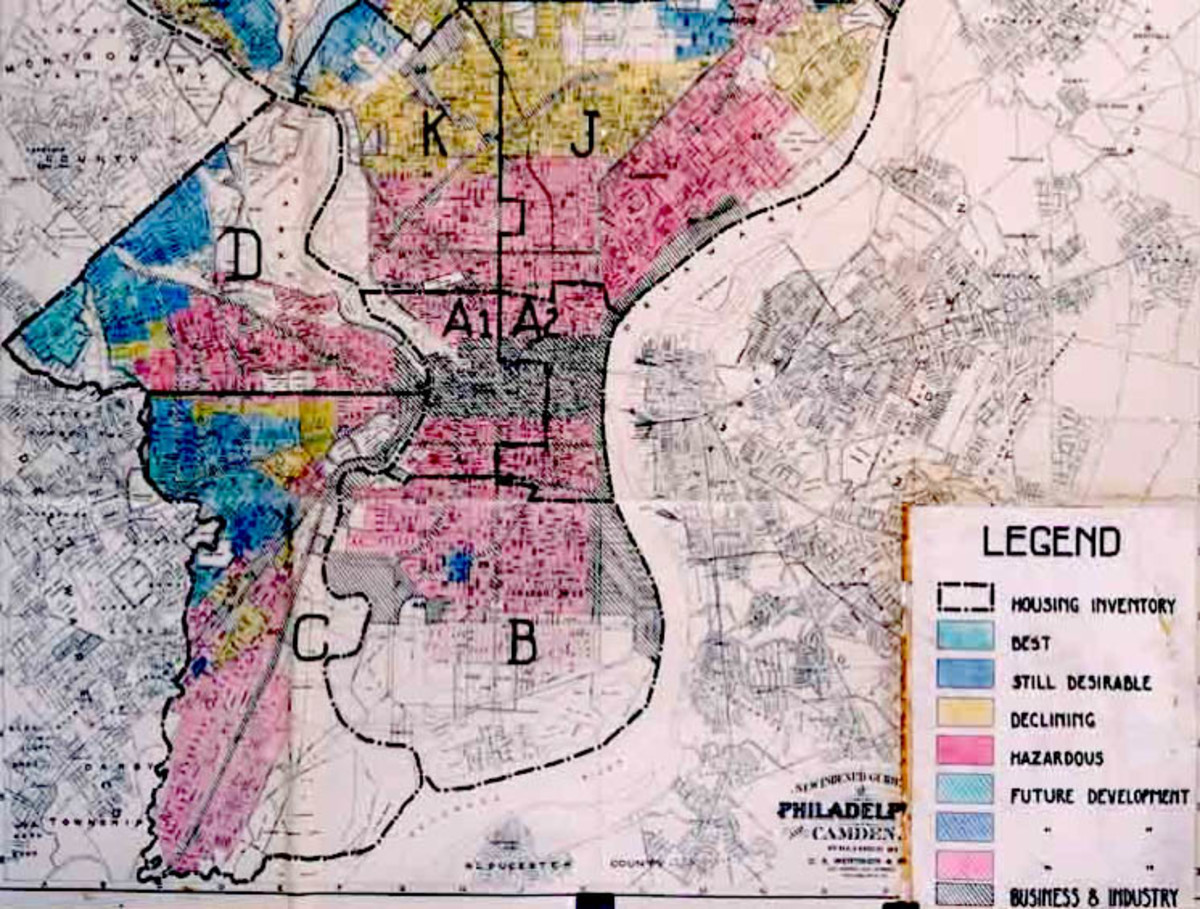

If you though Joseph Otting spent his entire two-and-a-half years as U.S. Comptroller of the Currency taking the “community” (read: uppity people of color who think they ought to have a say in things in their neighborhoods) out of the Community Reinvestment Act, think again: He also spent it making sure no bank would ever have to suffer the pain and embarrassment of public disclosure of racist lending practices, let alone a fine.

Since President Donald Trump took office, the OCC has quietly shelved at least six investigations of discrimination and redlining, according to internal agency documents and eight people familiar with the cases…. In each case, despite staff recommendations that fines or other penalties be imposed, the OCC took no public action and closed the investigations quietly….

The OCC has historically prioritized the well-being of banks over bank customers, said current and former examiners, but the balance has shifted even further under the Trump administration.