Hunger, rocketing inflation, power blackouts, fuel queues – Zimbabwe has been here before, but it’s been a decade since things were quite this bad, ever-resilient citizens in the capital, Harare, say.

The trigger for a sudden surge in prices came last month, when the US dollar was abandoned as legal tender, 10 years after Zimbabwe ditched its worthless local currency and dollarised as inflation hit 89.7-sextillion percent – that’s 20 zeroes.

The same ruling party is at the helm now as 10 years ago, noted Godfrey Kanyenze of the Labour and Economic Research Unit of Zimbabwe, a trade union-linked think tank. And that has added to the worries, he said, because few people trust it has the ability to steer the country out of the current mess – in which a third of the rural population is struggling to cover basic food needs.

Zimbabwe already faces a range of humanitarian concerns, with the UN and international aid groups filling gaps in food security, health and HIV care, water and sanitation, and social protection for vulnerable citizens.

“This is management by crisis,” Kanyenze told The New Humanitarian. The government is “pushing a mantra of ‘austerity for prosperity’, but it’s a government without a human face and it’s just knee-jerk reactions.”

The government says the decision to return to a single, Zimbabwean, currency is crucial to stabilising the economy.

John Kazingizi sells fruit and vegetables with his wife in Hatcliffe market, a high-density suburb of Harare. “What worries me most is prices keep increasing and my sales keep going down, as people are no longer buying as they used to,” he told TNH last week.

The couple struggle to find the money to buy a little fresh stock each day and meet their basic household costs – including repayments on a debt they took out to cover school fees for their five children. “We just need our economy to work again,” said Kazingizi.

The Zimbabwe Coalition on Debt and Development, a social and economic justice NGO, has argued that banning the US dollar and all foreign currencies will simply boost the black market.

“There is a need to address the root causes of the current currency crisis, which are rampant corruption, mismanagement of public finances, and impunity being enjoyed by those that are fuelling the crisis through arbitrage and resource haemorrhage,” the NGO noted in a press statement.

The central bank’s move has not put an end to strike threats, which likely helped prompt the government’s currency decision last month. The Zimbabwe Congress of Trade Unions is warning it will call a stayaway to protest the rising cost of living, although it has not yet set a date.

When the unions last led a work stoppage in January, following the sudden announcement of a fuel price increase of 150 percent, security forces shot dead 17 people and raped 17 women, according to Human Rights Watch.

Fuel prices have been hiked three-more times since January, with an average daily commute now costing as much as $20.

More of the same

President Emmerson Mnangagwa’s cash-strapped government had long insisted the Zimbabwe dollar would only be re-introduced when the economic fundamentals were right.

Yet with inflation almost hitting 175 percent for June, 18-hour power cuts, and 3.5 million people facing drought-induced hunger in the countryside, “the fundamentals are clearly out of whack,” noted Mike Chipere-Ngazimbi, economics researcher at South Africa’s University of Pretoria.

A disastrous harvest – with maize production just 45 percent of last season – has compounded the hardships. The World Food Programme aims to reach 1.2 million people with food aid, but by March next year an estimated 5.5 million will be unsure where their next meal will come from.

When Mnangagwa came to power 18 months ago after a military coup ended the 30-year reign of President Robert Mugabe, he promised reforms.

But Mnangagwa, a ruling party stalwart, has failed to deliver a programme attractive enough to investors or multilateral financial institutions, or win over a country shocked by the army’s violent enforcement of last year’s close-run election result.

The one bright spot in Zimbabwe’s recent economic history was a period of coalition government between Mugabe’s ZANU-PF and the opposition Movement for Democratic Change lasting from 2009-2013. Then, GDP growth ramped up to more than 9 percent – although overall poverty levels remained stubbornly high.

To rescue the country from hyperinflation, in which prices doubled almost daily, an early decision in 2009 did away with the Zimbabwe dollar in favour of a basket of foreign currencies. The downside was foreign currency shortages in an import-dependent economy where more dollars leave the country than arrive.

Since then, an ever-more creative series of currency policies have been put in place to address that problem.

Currency conundrums

In 2016, the government introduced bond notes and coins, supposedly worth the same as the US dollar. But they steadily lost value on the informal market – and became an immediate source of arbitrage profits for the well-connected.

The Mnangagwa government has encouraged adopting mobile money to reduce the need for physical cash. According to the reserve bank, mobile money was used for 85 percent of all retail transactions in the last quarter of 2018.

But high transaction fees and a 2 percent government tax makes mobile money expensive – further eroding people’s purchasing power. In the rural areas, where mobile money is the common payment system for livestock sales, people are turning to barter instead, according to FEWS NET, the USAID-funded early warning hunger monitor.

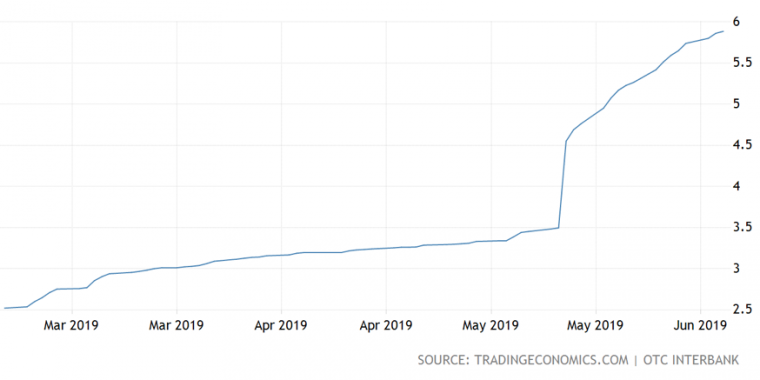

In February, as a step towards creating a local currency, the government introduced the Real Time Gross Settlement dollar, or RTGS – effectively a digital currency harmonising bond notes, mobile money, and debit cards tied to an official US dollar exchange rate.

Immediately, the RTGS dollar began to lose value on the parallel market.

“The economic situation makes us feel like orphans in our own country.”

Last month, the RTGS dollar was trading on the streets at about 13 to the US dollar, more than double the official interbank rate.

On 24 June, the government abruptly decreed that the country’s sole legal tender was the RTGS, renamed the Zimbabwe dollar, and abolished the use of multiple currencies. The aim was to end the informal market contributing to galloping inflation and restore government control over monetary policy.

Civil servants had been threatening to strike, demanding payment in US dollars, and there were reports the military was also unhappy with their RTGS denominated pay packets.

But the introduction of the Zimbabwe dollar has not halted its slide on the black market, and soon after the ban on the use of foreign currencies was announced, Finance Minister Mthuli Ncube said the tourist destination of Victoria Falls was exempted.

“It’s very clear the decision to move to a local currency was done in haste,” said Kanyenze of the labour think tank. “The economy was re-dollarising, and particularly the military were demanding to be paid in dollars.”

Kazingizi, the fruit and vegetable seller, said he sees little sign that things will improve any time soon. His wife gets up every day at 3 am to go to the market, he said, but the family still struggles to stay afloat.

“The economic situation makes us feel like orphans in our own country,” he told TNH.

Post published in: Business